Two companies, Chiang Wei and Euro American International Energy, according to an investigation by Radio Tamazuj, are long-term beneficiaries of and have been allocated South Sudan’s crude oil below prevailing market prices. They have been acting as speculators, middlemen, and commission agents who buy oil cheaply and sell it at a higher price and pocket the difference. This cannot happen without approval from the highest level in Juba, and is explained by the last-minute decisions to reverse and or reallocate cargoes to them.

Idris Taha, a Sudanese businessman, has been linked to firms, including Euro American Energy and Holdcorp, which have quietly gained control over a significant share of South Sudan’s crude oil exports and exploration, often operating outside traditional, transparent tender processes. His entities have been described as playing a key role in the “shadow economy” of South Sudan’s oil sector. Chiang Wei Ltd (also operating as Chiangwei Group) has been involved in oil-backed loans and cargo allocations in South Sudan. The company is Dubai-based and involved in offshore crude oil trading, project management, and food and beverages. The company has been linked to opaque oil deals in South Sudan, including receiving a $15 million “arrangers’ fee” related to a prepayment agreement with Sahara Energy Resources DMCC, according to Kenya Insights.

According to this publication’s investigation, in what appears to be a complicated syndicate involving very high-ranking officials in South Sudan who have the power to determine which company ‘buys’ the country’s oil below prevailing market prices, only to resell it at higher prices later. Also, the deliberate move to keep oil sales shrouded in secrecy is telling and meant to facilitate these illicit dealings.

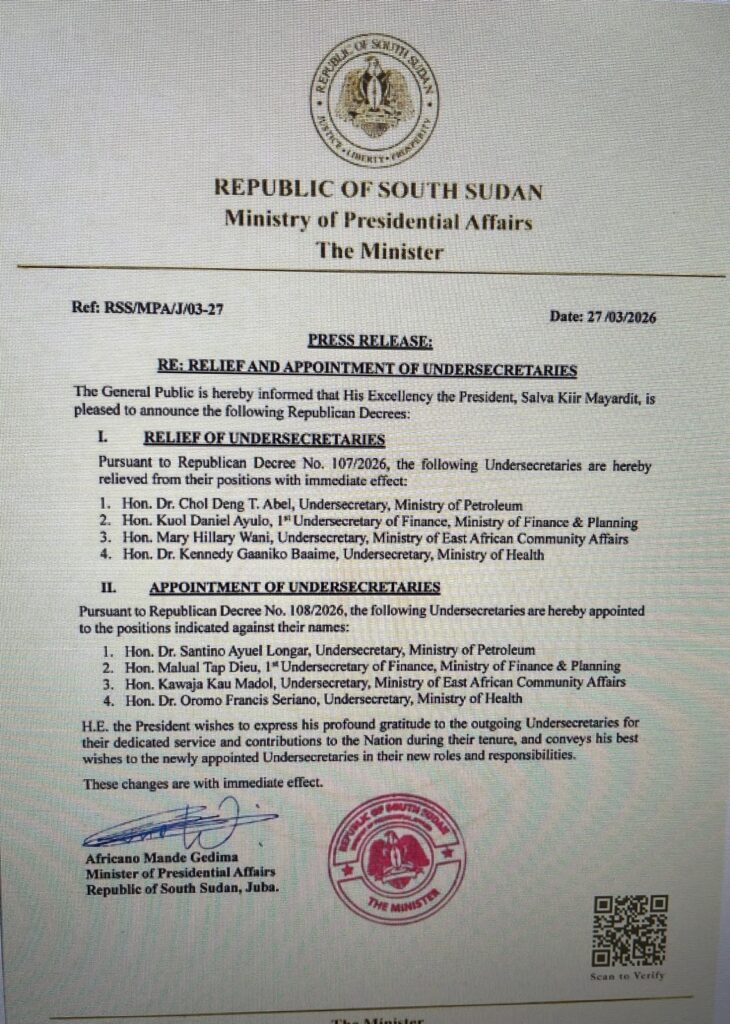

The removal of Dr. Chol Deng Thon Abel, the former Undersecretary for Petroleum, on 27 March 2026, has not resolved the controversy surrounding South Sudan’s crude oil allocations. Internal documentation reviewed during this investigation indicates the persistence of a system structured around a limited number of recurring actors—primarily Chiang Wei and Euro American International Energy—where last-minute decisions, repeated allocation patterns, and pricing mechanisms appear to systematically disadvantage the state.

Dubious allocations

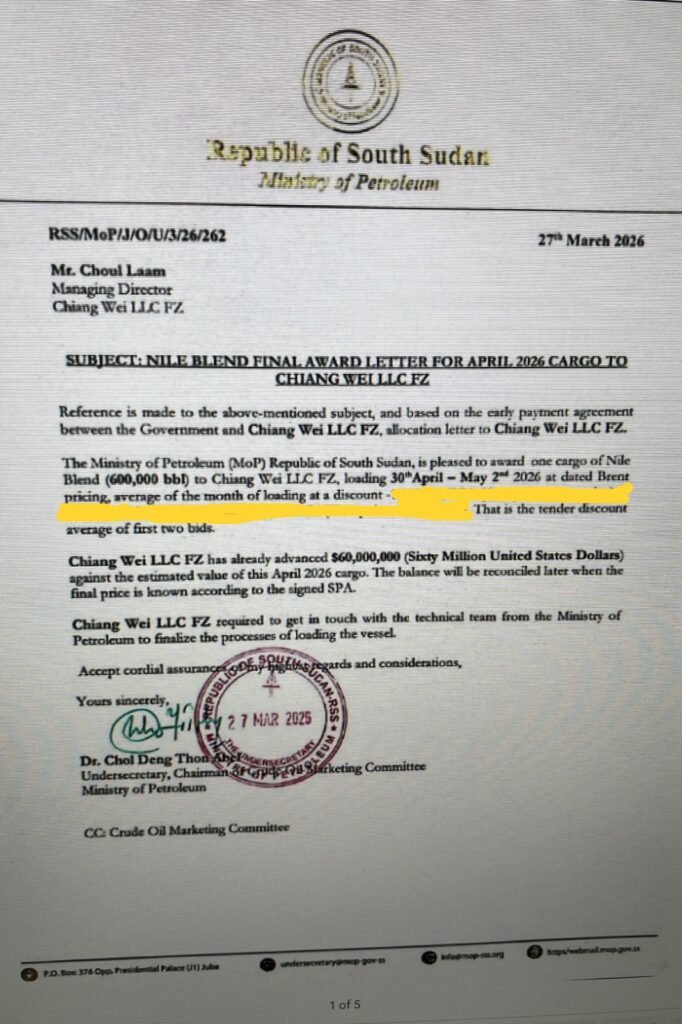

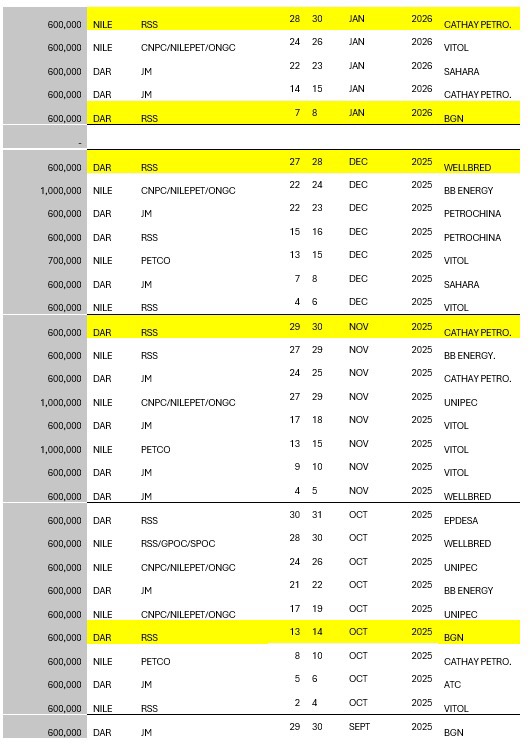

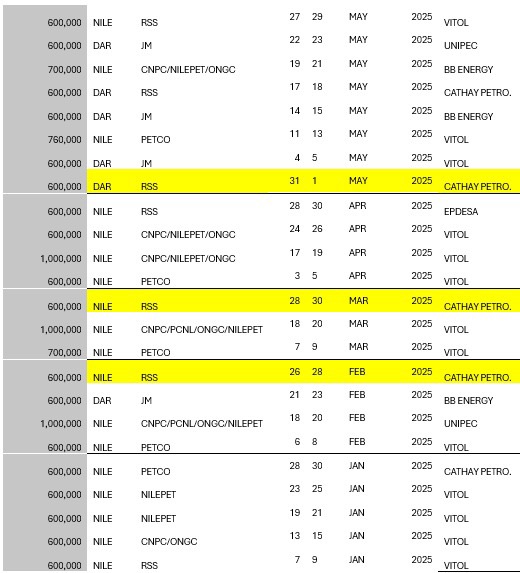

South Sudan remains heavily dependent on oil revenues, yet part of the value generated appears to be diverted through a network of intermediaries and pre-financing arrangements. Internal records [attached below] consistently identify the same entities at the center of allocations: Chiang Wei, Euro American International Energy, Cathay Petroleum, and BGN. A key distinction emerges between allocation beneficiaries and actual off-takers. Chiang Wei and Euro American International Energy frequently appear as beneficiaries of cargoes without necessarily acting as final buyers. Their role appears to consist of controlling access to cargoes by securing allocation letters, locking in pricing formulas, arranging pre-financing, and subsequently transferring or assigning the lifting to other entities with operational capacity. Companies such as Cathay Petroleum and BGN tend to appear at this second stage, handling operational or commercial execution. In this structure, margins are captured upstream, before physical loading.

Chiang Wei is identified in the documents as a central corporate actor rather than a peripheral participant. The company appears repeatedly in sensitive cargo allocations, particularly those approved at the very end of officials’ mandates. Despite the dismissal and arrest of senior figures associated with a previous opaque allocation system, both Chiang Wei and Euro American International Energy continue to feature prominently across allocation records.

End of tenure allocations

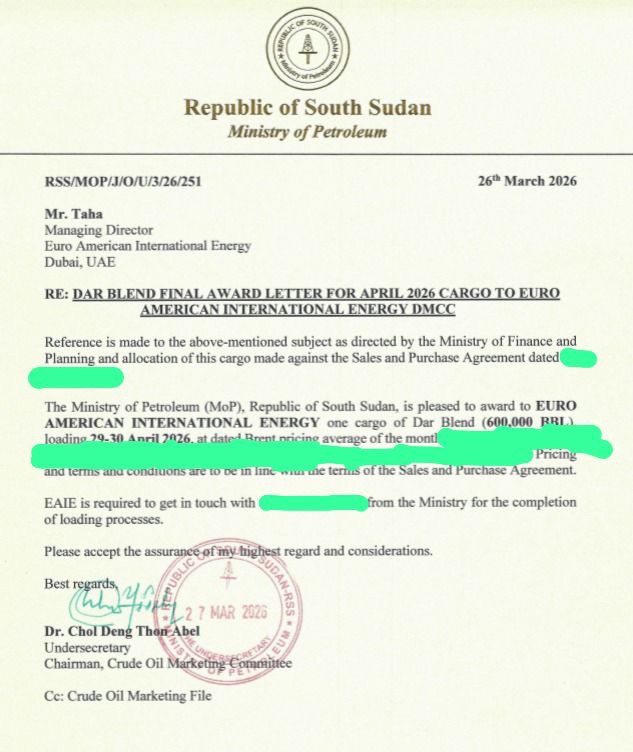

The timing of allocations is a critical element. On March 27, 2026, an official decree signed by Africano Mande Gedima, Minister of Presidential Affairs, confirmed the departure of Dr. Chol Deng T. Abel and the appointment of Dr. Santino Ayuel Longar as his successor. On that same day, immediately before leaving office, Dr. Chol signed allocation letters granting cargoes to Chiang Wei and Euro American International Energy. This effectively secured their position at the point of administrative transition.

This pattern of end-of-mandate decisions is not isolated. Other officials, including Deng Lual and Bak, also approved cargo allocations on their final day in office, repeatedly benefiting the same group of actors.

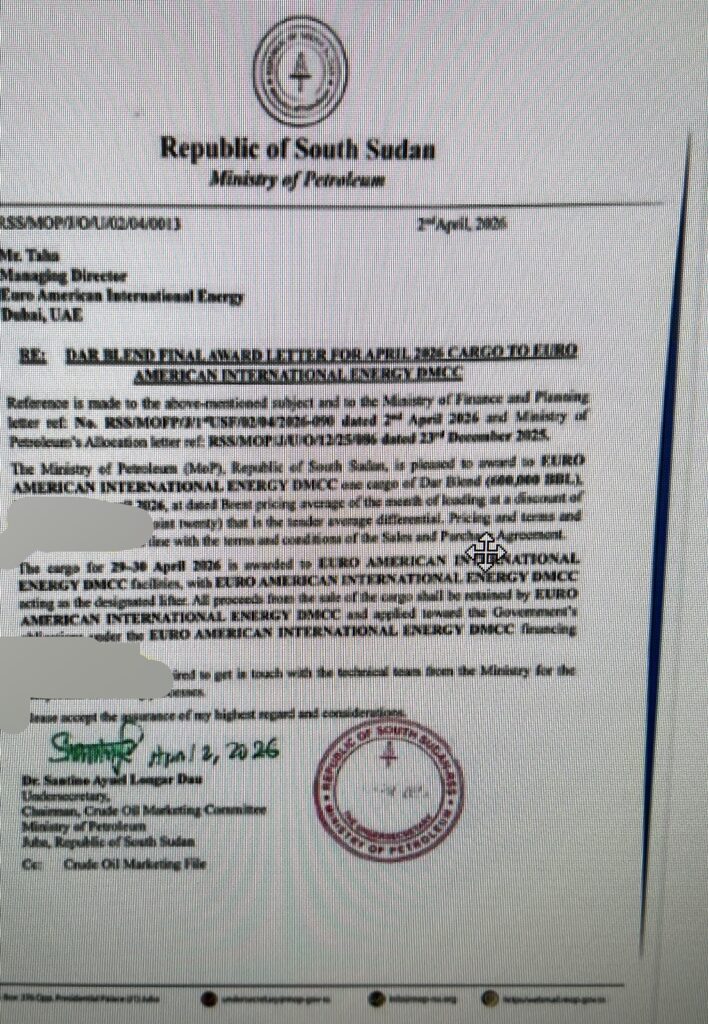

The April 2026 Dar Blend cargo illustrates the mechanism in detail. A shipment of 600,000 barrels, scheduled for loading on April 29–30, 2026, was initially allocated to Euro American International Energy on March 27 by Dr. Chol. On March 31, Dr. Santino Ayuel Longar reassigned the same cargo to Trinity Energy Limited as part of a debt-servicing arrangement linked to Afreximbank. Trinity was designated as a lifter, with proceeds to be retained by Afreximbank for government debt obligations. However, on April 3, 2026, a further letter attributed a cargo of identical volume and loading schedule to Euro America International Energy DMCC. In this document, Euro American International Energy reappears as lifter, with authority to retain proceeds for application to government financing obligations.

Within less than one week, the same cargo appears to have moved through three separate allocations: EuroAmerican on March 27, Trinity on March 31, and again EuroAmerican on April 3. If these documents refer to a single cargo, this raises unresolved questions regarding effective control, beneficiary entitlement, and the legal basis of allocation decisions.

Intermediaries and allies benefit from undercut pricing.

Beyond allocation sequencing, pricing mechanisms represent a major financial issue. Internal documents indicate that at least one cargo lifted in March 2026 was priced using February benchmarks, when crude traded at approximately 70 to 72 dollars per barrel. Shortly thereafter, following U.S. and Israeli strikes on Iran, global oil prices rose sharply to between 100 and 110 dollars per barrel. Under such conditions, South Sudan appears to have been paid at around 70 dollars per barrel, while the same cargo could be resold above 100 dollars.

On a 600,000-barrel cargo, a 30-dollar differential represents approximately 18 million dollars, while a 40-dollar differential represents approximately 24 million dollars. These margins appear to accrue to intermediaries and oil sector decision-makers in Juba rather than to the state. The documents suggest the use of pricing clauses or options enabling the application of earlier, lower benchmarks to cargoes lifted in a rising market. This allows intermediaries to capture market upside while the state is paid as if prices had remained unchanged. Similar mechanisms may apply to other cargoes currently under allocation.

These pricing arrangements are less visible than direct per-barrel discounts, as they are embedded within contractual structures. However, their economic effect is comparable or greater, resulting in the diversion of oil value at a time when increased global prices should strengthen public finances. This occurs in a context where government entities reportedly face ongoing difficulties meeting salary obligations.

Layered contractual instruments

Euro American International Energy’s repeated reappearance across allocation documents, particularly during administrative transitions, suggests the use of layered contractual instruments. Incoming officials inherit commitments formalized shortly before their appointment through allocation letters, cancellations, or restructuring agreements. These overlapping documents create competing claims that are difficult to unwind, enabling actors such as Euro American International Energy, owned by Idris Taha, to regain effective control over cargoes even after formal reassignment.

The April cargo sequence illustrates this dynamic: despite reassignment to Trinity Energy under a structured Afreximbank arrangement, subsequent documentation appears to restore control to Euro American International Energy. The formal administrative sequence is therefore less determinative than the outcome, in which the same beneficiary re-emerges.

The financing maze

A compliance report dated 9 March 2026 raises additional concerns regarding Chiang Wei’s operational structure. According to this report, WellBred Trading DMCC provides financial backing to Chiang Wei LLC FZ, which then participates in South Sudan crude allocations. The report also indicates that Chiang Wei conducted RMB-denominated transactions with Shandong Hi-Speed Group in connection with oil cargo operations, and refers to potential links with financial flows associated with Iranian oil networks under sanctions.

While these elements remain allegations requiring further investigation, the report outlines a potential model in which Chiang Wei secures allocations, arranges lifting and resale, and may retain part of the proceeds rather than fully transferring them to the South Sudanese state. The report recommends suspending commercial relations with Chiang Wei LLC FZ pending a financial investigation.

Two principal concerns arise from this structure. First, that pricing mechanisms enable the capture of differences between February and March market levels. Second, the financing and resale structure may operate as a closed loop, in which part of the oil’s value is recycled into subsequent transactions, limiting the proportion of revenue reaching the state.

The financial implications for South Sudan

The implications for South Sudan are significant. Revenue losses linked to pricing discrepancies directly affect public finances at a time of elevated oil prices. At the same time, reliance on actors such as Chiang Wei and Euro American International Energy exposes the country to risks, including sanctions scrutiny, trade-based money laundering, and potential diversion of sovereign revenues.

Despite leadership changes within the Ministry of Petroleum, the underlying allocation system appears unchanged. Structural reforms would require the publication of allocations, the identification of ultimate beneficiaries, the implementation of competitive tendering, the alignment with market-based pricing, the use of escrow accounts, and the independent auditing of allocation processes.

As long as Chiang Wei and Euro American International Energy continue to dominate cargo allocations through opaque and contested mechanisms, control over South Sudan’s oil revenues remains unclear. The central unresolved issue is that although the state formally owns the oil, the same actors continue to capture its value through opaque structures that remain difficult to trace or challenge.

Who makes the final allocation decision?

A source knowledgeable about the allocations and other dealings, who preferred anonymity due to fear of reprisals, told Radio Tamazuj that the final decision on allocations and cargoes is made by South Sudan President Salva Kiir and his security advisor, Tut Gatluak.

“Tut Gatluak Manime makes the final decisions on oil allocations, cargoes, appointments, and removals, particularly when the President is tired, unwell, or outside the country, much to the frustration of the Undersecretary of Petroleum and the Minister of Finance,” he stated.

Notice of Correction: The initial version of this story stated that Chiang Wei Ltd, also operating as Chiangwei Group, was partly owned by Kueth Duany. This was inaccurate. Mr. Duany has not been an owner of Chiang Wei Ltd since 2021, following a transfer of ownership.

This story was updated at 10:54 a.m. CAT on Thursday, 14 May 2026.

Radio Tamazuj apologises to Mr. Duany for any inconvenience this may have caused.

and then

and then